An income summary is a term used in accounting to describe how income moves between the revenue and cost account, thus closing the accounting process. In this article, we’ll go through the income summary account in-depth and show you how to close it.

What is an Income Summary Account?

The income summary account is a temporary account into which all income statement revenue and expense accounts are placed at the end of an accounting period. The net amount put into this account equals the business’s net profit or loss for the period. Shifting revenue out of the income statement, therefore, entails debiting the revenue account for the total amount of revenue recorded in the period and crediting the income summary account.

Similarly, transferring expenses off the income statement necessitates crediting all expense accounts for the whole amount of expenses incurred during the period and debiting the income summary account. This is the initial step in using theaccount.

If the resulting balance in the account is a profit (a credit balance), debit the income summary account and credit the retained earnings account to shift the profit into retained earnings. If the resulting balance in the account is a loss (a negative balance), credit the income summary account for the loss and debit the retained earnings account to move the loss into retained earnings. This is the second stage in using the income summary account; the account should now have a zero balance.

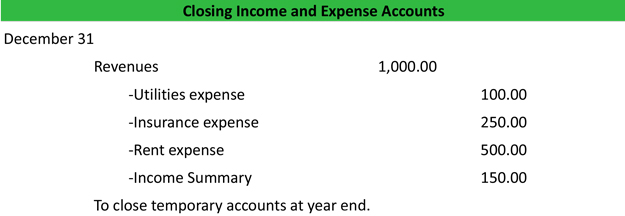

Example

At the end of a period, the balances of all income and expense accounts are transferred to the income summary account. This retains these balances until final closing entries are made. The income summary account is then canceled out. Afterward, its balance is transferred to the retained earnings (for corporations) or capital accounts (for partnerships). This moves income or loss from an income statement account to a balance sheet account.

The income summary account is only used at this point. It has a zero balance for the rest of the year. Here are some examples of closing statements. The income and spending accounts are, as you can see, transferred to the income summary account.

After the income statement is created, the final income summary balance is transferred to retained profits or capital accounts. This income balance is subsequently reflected in the balance sheet’s owner’s equity section.

What is the Purpose of the Income Summary Account?

The income summary account acts as a stopgap. Thus, accumulating revenue and spending totals before the resulting profit or loss is passed through to the retained earnings account. As a result, the account is not necessarily required. It can, however, provide a useful audit trail by demonstrating how these aggregate amounts were carried through to retained earnings.

How to Make an Income Summary

#1. Close Revenue Accounts

Credit balances are always present in revenue accounts. All revenue accounts will be closed at the conclusion of the accounting period. We do this by transferring the credit amount to the income summary. The revenue accounts will be debited, and the income summary account will be credited. All revenue accounts will become zero after this entry is completed.

#2. Close Expense Accounts

Expense accounts always have a negative balance. All fees will be closed at the end of the accounting period. We also do this by transferring the debit to the income summary by crediting the costs account and debiting the income summary account. Following the completion of this entry, the balance of all expense accounts will be zero.

#3. Complete the Income Summary Account

All of the revenue accounts balance in the credit side column as the organization’s total income. Also, all of the expense accounts balance in the debit side column as the organization’s total spending. If the credit balance is greater than the debit balance, the profit is indicated. On the other hand, if the debit balance is greater than the credit balance, the loss is indicated. Whatever remains in the last credit or debit balance will be transferred to the balance sheet’s retained profits or the capital account. The income summary will then be closed.

Advantages

- It consolidates the organization’s overall revenue and cost data into a single location.

- It assists investors and shareholders in determining future investments by analyzing a company’s financial performance over a certain time period.

- One may readily track the company’s performance by checking the income summary from previous years to see if it is consistently profitable.

- It also aids in the completion of income tax forms by providing all relevant information in one location.

- It is simple to grasp because it only has two columns.

- Income summary aids in the investigation of budget vs. actual variance.

- It is simple to calculate the cash profit by adding or subtracting the accrual balances.

Disadvantages

- It covers revenue and expenses from both operations and non-operations. As a result, it does not provide an accurate financial picture of the organization.

- It is prepared on an accrual basis. This means that it records the total sales value, whether or not money has been received, expenditures have been recorded on an accrual basis, and whether or not it has been paid. As a result, there is a possibility of misrepresentation.

- A one-year income summary is useless for analyzing financial performance. For analyzing financial performance, an investor must take at least ten years of summary. As a result, obtaining the organization’s ten-year summary, which is not listed, is time-consuming and often difficult.

How to Close an Income Summary Account

There are two ways to close temporary accounts. You can either close these accounts straight to the retained profits account or close them to the income summary account.

Closing temporary accounts to the income summary account requires an extra step. However, it also gives an audit record of the year’s revenues, expenses, and net income.

The balances in the temporary accounts are retained in the income summary account until final closing entries are completed. This serves as a valuable error check. Once all temporary accounts have been closed, the balance in the income summary account should equal the company’s net income for the year.

The income summary account is then canceled out and its balance is transferred to the retained earnings (for corporations) or capital accounts (for partnerships). This moves income or loss from an income statement account to a balance sheet account. The income summary account is only used at this point. The income summary account has a zero balance for the rest of the year.

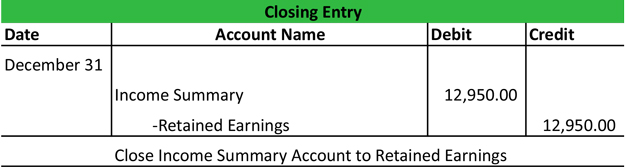

Example

The income summary account has a balance equal to Sam’s Guitar Shop’s net income for the year after Sam’s Guitar Shop prepares its closing entries. In a journal entry like this, the balance is transferred to the retained earnings account.

Following this entry, the balance of all temporary accounts, including the income summary account, should be zero.

Sam’s books are now totally closed for the year, and he may create the post-closing trial balance and reopen his books with reverse entries in the following steps of the accounting cycle.

What Is the Difference Between an Income Summary and an Income Statement?

At the end of each accounting period, businesses prepare an income summary and an income statement. An income summary is a clearing account that is used to close income-statement accounts at the conclusion of a period, whereas an income statement is a financial statement that is generated based on the accounting records of income-statement accounts recorded earlier in the period. In other words, an income summary zeros out the balances of income-statement accounts in accounting records for next-period recording, but an income statement reports the balances of income-statement accounts to show current-period performance.

Income Summary

At the end of an accounting period, the account of income summary is utilized for closing-entry recording. Account balances of income-statement accounts, specifically revenues and costs, are closed and reset to zero at the end of an accounting period to prepare them for transaction recording in the next month. Companies record revenues and expenses on a quarterly rather than continuous basis, and account balances from one period are not added to those from the next.

Transfer of Earnings

Debit all revenue accounts to offset existing revenue balances and credit income summary to reset revenue balances to zero. To zero off current expense balances, debit the income summary and credit all expense accounts. After closing the account of income summary with the amount of revenues and expenses, the net amount, or the difference between revenues and expenses in the income summary, is transferred to the account of retained earnings with a debit to income summary and a credit to retained earnings. The earnings transfer also closes the income summary account.

Profit and income Statement

While revenues and expenses in accounting records are reset to zero at the conclusion of a period, they are reported in the income statement to reflect profitability for the time. An income statement is a list of all revenue and expense accounts classified according to the type of revenue and expense. In general, revenues and expenses are derived from operating activities, which include both ongoing and discontinued operations, non-operating activities, such as investments and other secondary activities, and any uncommon or extraordinary activities.

Profitability Analysis

An income statement’s objective is to compile all of the account information on revenues and expenses recorded during an accounting period and display it in standard income-statement format. An income statement assists users in evaluating a company’s previous performance and offers a foundation for forecasting future success. Information on various components of total net income, as a result of revenues and expenses from various business operations, is especially valuable in estimating the risk of not achieving a specified level of income in the future. A high level of total current income, for example, combined with a relatively low level of income from the major operating activities may imply reduced total income in the future.

Conclusion

An income summary is a summary of income and expenses for a certain period, with the result being profit or loss. It is a necessary instrument for the preparation of financial statements. It acts as a checkpoint and reduces errors in financial statement preparation by directly transferring the balance from revenue and spending accounts.

Instead of transmitting a single balance for each account, it aggregates all ledger balances into a single value and transfers it to a balance sheet, producing more meaningful results for investors, management, vendors, and other stakeholders. On one page, it outlines all of the company’s operating and non-operating business activities and concludes its financial performance.

Frequently Asked Questions

What kind of account is income summary?

The income summary account is a temporal account.

How do you record income summary account?

You record the income summary amount by adding the total expenses and total income and then transferring them to the balance sheet.